While we haven’t yet said goodbye to 2023, it’s not too early to begin thinking about any tax changes that may be on the horizon.

The Tax Cuts and Jobs Act (TCJA) of 2017 was designed to overhaul the federal tax code by reforming individual and business taxes. As a result, sweeping tax changes lowered marginal tax rates and the cost of capital.

Although some of these provisions are permanent, most individual tax changes are not. Unless Congress acts, many of the changes implemented are scheduled to “sunset” on December 31, 2025. At that time, rates will revert to pre-2017 levels.

Knowing what changes may be coming and preparing for this new reality may be an excellent first step. There may be actions you can take to prepare for what may happen next.

Here’s a summary of the TCJA-related changes expected for each quarter leading up to the 2025 sunset of the TCJA.

Remember that this article is for informational purposes only and is not intended as a replacement for real-life advice, so consult your tax, legal, or accounting professional before modifying your strategy in anticipation of TCJA-related adjustments.

Remember: tax laws are constantly changing, and there is no guarantee that all the provisions of the TCJA will expire.

Overview of the Tax Cuts and Jobs Act in 2017

When the TCJA was passed in 2017, it lowered most individual income tax rates—including the top marginal rate—from 39.6 percent to 37 percent. The law maintained the preexisting seven-bracket rate structure but updated income thresholds. The TCJA also increased the standard deduction to $12,400 for single filers and $24,800 for married filers versus $6,500 (single) and $9,550 (married) under the prior code.

To offset some associated costs, the TCJA eliminated the personal exemption and various other miscellaneous deductions and limited certain itemized deductions, like the state and local tax (SALT) deduction. The TCJA also increased the Child Tax Credit (CTC) from $1,000 to $2,000—the first $1,400 of which was refundable—and raised the associated income threshold from $110,000 to $400,000.1

The TCJA lowered the corporate income tax (CIT) rate for businesses from 35 percent to 21 percent starting in 2018. The measure also allowed for the full and immediate expensing of short-lived capital investments for five years and increased the Section 179 expensing cap from $500,000 to $1 million. Furthermore, the bill eliminated or curtailed various business taxes and expenditures, including the deductibility of net interest, net operating loss carrybacks and carryforwards, and the corporate alternative minimum tax (AMT).1

The TCJA Lowered Average Tax Rates for All Income Groups

What’s Scheduled to Change for Individuals

Tax Rates

The reduction in tax rates for individuals and married couples in 2017 may increase back to where they were in 2016. That means that after December 31, 2025:

- The 37% rate is scheduled to revert to 39.6%

- The 24% rate is scheduled to revert to 28%

- The 22% rate is scheduled to revert to 25%

- The 12% rate is scheduled to revert to 15%

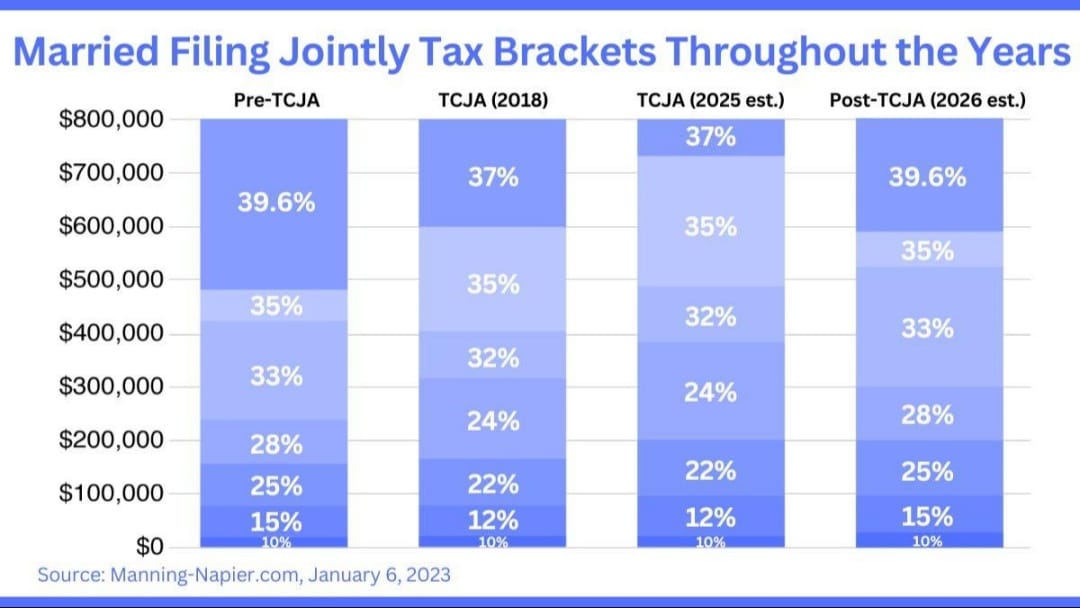

Tax Brackets

The tax brackets you fall into based on your income may also go back to the broader ranges that were in effect before the TCJA. Below is a visual of how much tax brackets changed 2018 for married joint filers and an estimate of their reversion in 2026.

Estate & Gift Tax Exemption

Under the TCJA, the federal lifetime estate and gift tax exclusion will increase from $12.06 million in 2022 to $12.92 million in 2023. Inflation could also increase in both 2024 and 2025. However, these higher levels are only temporary. Like other provisions in the TCJA, the estate and gift tax exclusion increase will sunset after 2025, setting the exclusion back to its pre-2017 level of $5 million, adjusted for inflation.2

Standard Deduction & Personal Exemptions

The TCJA eliminated the personal exemption ($4,050) and doubled standard deductions, adjusting for inflation each year. The standard deduction for single filers increased from $6,350 to $12,000, and that for married filing jointly filers increased from $12,700 to $24,000. This increase resulted in fewer people itemizing deductions. After the standard deduction peaks in 2025 and is cut back in half in 2026, itemizing may become much more appealing to many filers.

Qualified Business Income

One of the most substantial changes introduced by the TCJA was the qualified business income deduction, which allowed for a tax deduction of up to 20% of business income for sole proprietors, LLCs, partnerships, S corps, trusts, and estates. The main reason for this deduction was to match the significant (and permanent) C-Corp tax rate reduction that was also put in place under the TCJA. Taxpayers with AGIs below $170,050 (single) or $340,100 (married) qualify for the full 20% deduction with a complete phase-out at $220,050 or $440,100, respectively. If not extended, this provision will go away as of 2026.

Alternative Minimum Tax (AMT)

The AMT has been the bane of many taxpayers’ existence. Originally intended to impact only the extremely wealthy and never indexed for inflation, it has trapped more and more middle-income taxpayers ever since.

The AMT received a significant makeover under the TCJA, with an exemption that increased from $54,300 to $70,300 for individuals and from $84,500 to $109,400 for married couples. More substantially, the income exemption phase-out increased from $120,700 to $500,000 for individuals and $160,900 to $1,000,000 for married couples. These changes reduced the number of AMT taxpayers from 5 million to only 200,000. With the sunsetting of the TCJA, AMT provisions will also revert.

Keeping You on Track

Preparing your taxes can be complex, and accidental errors can be easy. By being diligent, carefully strategizing, and keeping up with new rules, you can improve your ability to manage your taxes and keep pace with whatever comes down from Washington. Remember: even if you’re working with a tax professional, you are responsible for correctly filing your financial details.

If you have any questions about your financial life, we’re here to help you navigate this evolving landscape as the TCJA expires. We always welcome collaborating with your tax professionals to align any strategies you take across your financial priorities.

1. TaxFoundation.org, August 30, 2023

2. ThinkAdvisor.com, August 30, 2023